On June 1, Moody's Investors Service announced a change to their global real estate market outlook (GREM). Their GREM outlook was changed from stable to negative. Perhaps to be expected from a ratings agency, the report focuses on REIT and REOCs' credit, although smaller private equity investors will likely find the report insightful.

The report notes a few interconnected factors leading to this downgrade: tighter credit markets, rising cost of capital, and declining property valuations. While some points, such as the projection that office and retail will face the most trouble (I could've told you that in June 2020), probably didn't require a professional analysis, the data driven insights go beyond simple speculation and allow investors to understand the hard numbers behind the intuition.

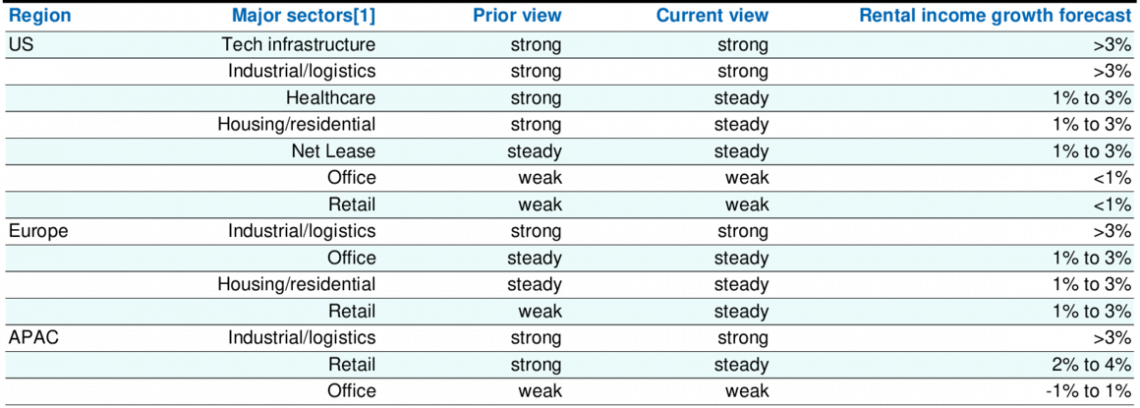

Industrial investors will be relieved to see their areas' outlooks remain strong (if they're not already on a boat paid for by their promote)Source: Moody's Investors Service

Industrial investors will be relieved to see their areas' outlooks remain strong (if they're not already on a boat paid for by their promote)Source: Moody's Investors Service

The report notes the US-specific risk of regional bank troubles. Regional banks are a key player in most CRE transactions, especially for non-institutional investors. Since the US makes up 76% of Moody's' GREM index, this is a substantial factor in the report. Local investors will likely find the report's US-specific risks to be relevant to them.

Some highlights include:

- Rent growth unlikely to offset higher cost of capital

- Cuts to discretionary spending may cause retail to struggle. This includes retail operations that recovered or were insulated from COVID effects

- REITs, whose tax structure forces a large dividend payout ratio, and REOCs with few cash reserves may find affordable debt difficult to come by

- REITs face the risk of low asset values if forced to liquidate parts of their holdings

- Rising rates across the board put debt coverage in jeopardy, further increasing risk and driving cost of capital even further up

- Class A office will likely not struggle to the extent of lesser assets

- Low vacancy for industrial, logistics, and tech infrastructure should bolster rent growth and valuations

Despite short-term headwinds, real estate markets will likely recover, although perhaps not at the sky-high valuations brought on by near-zero interest rates. More than a decade of unprecedented low inflation and low rates may cause hardships for highly levered owners, especially if their underwriting called for strong rent growth.

For opportunistic investors with dry powder on the sideline, there may be tremendous opportunity to pick up assets at a discount due to liquidations or foreclosures. Equity IRR can be boosted by adding debt to the capital stack once markets stabilize. The tricky part is timing: how much do you trust the SOFR swap curve?